Operating conditions are worse than anyone projected. Affordable housing properties are not set up to adjust.

It’s an extraordinarily challenging time to operate affordable housing. Community-based owners are struggling to deal with ballooning expenses, unpaid rent, property management staffing shortages, and residents with high levels of need who lack adequate support.

It’s not just an Oregon problem. National lenders and investors are raising red flags, and data from across the country shows that properties everywhere are stumbling. Among other grim statistics that national housing investor/owner Enterprise reported last summer, 29% of properties in its portfolio experienced negative cash flow in 2022—requiring massive increases in cash advances from owners.

As an industry, we need to shine a light on the challenges facing housing operations today and build our understanding of root causes, impacts, and possible antidotes. But first, let’s take a closer look at what we’re seeing on the ground.

Fast-growing costs

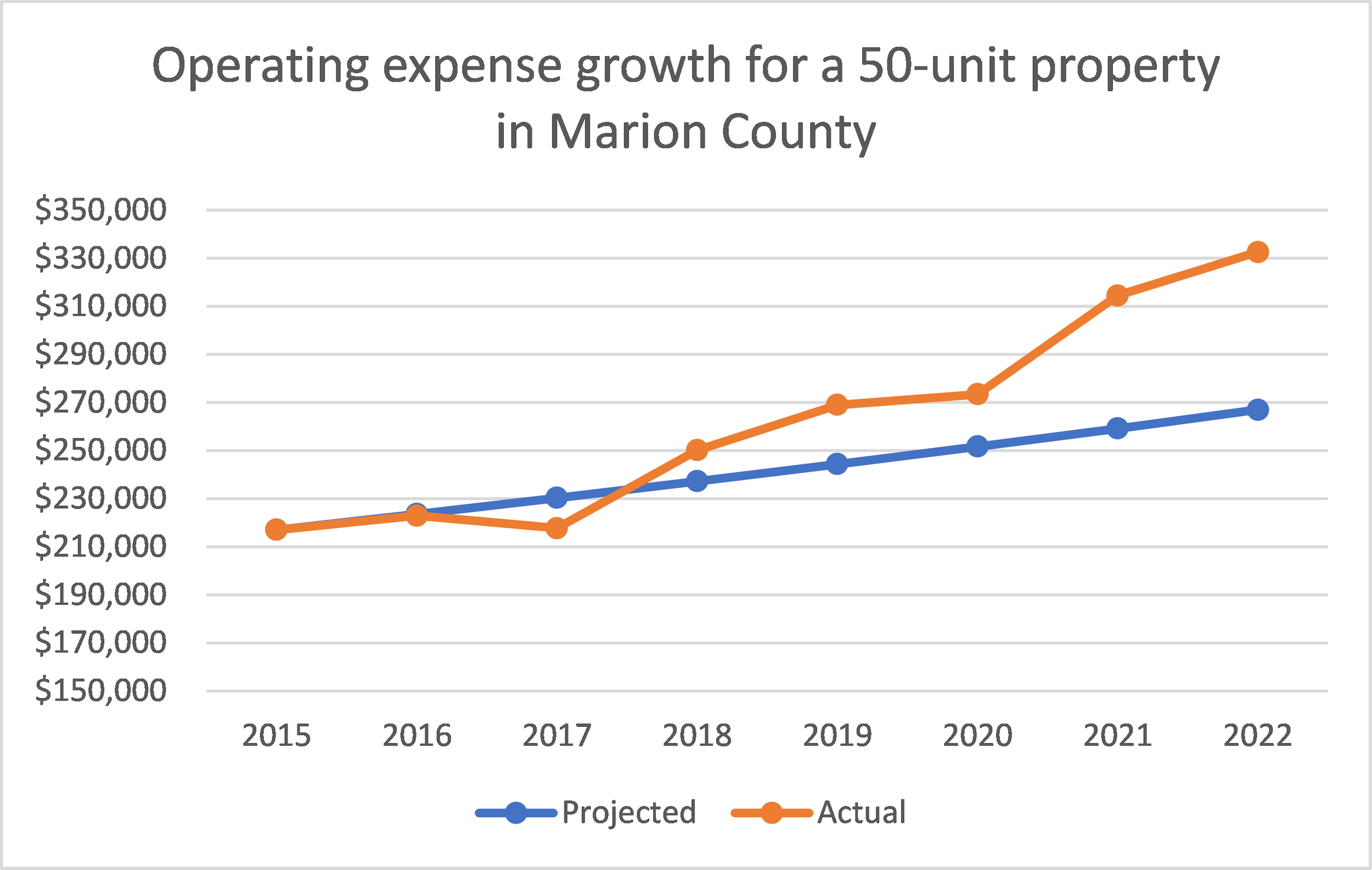

In 2015, real estate industry experts were projecting 3.0% annual growth in multifamily property operating expenses. Instead, costs at Oregon properties zoomed up at a median annual rate of 4.0% in the seven years from 2015 to 2022, according to CohnReznick’s 2023 Affordable Housing Credit Study.

Cumulatively, that annual 1.0% difference had a big effect; expenses increased 31.6% over seven years, far more than the 23.0% most owners were projecting. In many Oregon counties, expenses grew even faster—averaging 5.51% growth per year in Marion County and 6.46% in Multnomah County.

Operating expenses for an average 50-unit apartment building in Marion County reached $332,500 in 2022—up 53% since 2015, or more than double the expected increase, assuming 3.0% annual growth.

The rapid expense growth has occurred across multiple cost areas, with varied factors fueling the increases. For instance, general price inflation and a rise in extreme weather events has driven up utility costs and repairs-and-maintenance costs, the largest cost center for many properties. Changing risk assessments in light of climate change and the pandemic have propelled skyrocketing property insurance premiums.

The list goes on, but what’s important to note is that nearly all key drivers of cost growth are outside of owners’ control. These aren’t the kinds of cost issues that can be mitigated by, say, fixing leaky water pipes or looking for a less expensive vendor. They are systemic.

Lagging revenue

How fast are costs growing? Faster than inflation and—more importantly—faster than revenues grew at typical properties during the same period.

In contrast to cost growth, revenue growth for many affordable housing properties has lagged projections. An unusually large number of properties are reporting revenue shortfalls as early as their first year of operations. As with cost growth, a combination of social, economic, and policy shifts outside of owners’ control are contributing to this slow-down.

Many owners delayed rent increases and paused evictions during the pandemic. The pandemic has subsided, but the financial losses and cash-flow problems resulting from foregone rent payments and foregone rent increases are only partially reversible in the short term, because of legal and contractual restrictions on the pace of rent hikes.

Despite slow rent increases, nonpayment of rent continues to be a problem. Owners are reporting increasingly large unpaid rent balances, longer turnover and vacancy timelines, and higher losses associated with evictions for nonpayment of rent. Adding to the weight of these problems, chronic staffing issues, caused by systemic under-resourcing of property and asset management functions, are hindering owners’ ability to provide effective property financial oversight.

Property management issues

Property management is becoming a bigger job. Properties can’t afford to pay for the full scope and level of property management services they need, partly because project-funding restrictions limit allowable expenditures. As a result, most portfolios are dealing with significant property management challenges.

Reported problems include high staff turnover, third-party service models that are not culturally responsive, providers that are unable to perform essential tasks, and financial reports that are delayed and/or inaccurate. Moreover, there is a shortage of property management services in the market.

Addressing a growing crisis

Importantly, the ability of affordable housing properties to earn income and accumulate reserves is legally and contractually restricted. To steward public investments and keep rents low, new developments are intentionally launched with just enough resources to pay the bills. When operating conditions turn out to be dramatically worse than projected, affordable properties cannot easily adjust.

This is precisely what is happening today: a large gap has opened between the conditions owners and underwriters projected (using thoughtful and reasonable assumptions) at the time of project financing versus conditions that exist today. Under these circumstances, the financial distress spreading through Oregon’s affordable housing portfolio will inevitably continue.

To stem the damage, increasing preservation funding is high on the list of strategies that must be considered. Other potential solutions include expanding or replicating the metro-area Risk Mitigation Program to support additional units (as is currently under discussion at the state level); and increasing the availability of, and caps on, Metro’s Supportive Housing Services funding to raise staffing levels and wages of resident services staff. Regulating the insurance industry, including public oversight of premiums and availability of coverage, should also be part of the conversation.

At HDC, we are committed to working with all partners to address this challenge. Flexibility, creative thinking, and collaboration will be critical to get distressed properties back on track. Diverse perspectives, including those of developers, property and asset managers, and resident advocates, in addition to owners and funders, will be needed to understand root issues and daylight available solutions. We will continue to report out on our work and share what we learn.